")

This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

A couple of years ago, the quarterly refunding announcements (QRA) from the Treasury Borrowing Advisory Committee (TBAC) were dry and boring meetings that only dorks like myself paid attention to. The TBAC advises the Treasury on debt issuance strategy for the upcoming quarter.

Ever since rates came off zero and fiscal deficits exploded, however, market participants have started to pay close attention to how the government is funding itself. Supply and demand are drivers of US Treasury yields. Therefore, if more supply is coming onto the long end of the yield curve, that will have a tangible impact on market prices.

This week, we received the last QRA before the election. With the caveat that anything from January 2025 onwards assumes a continuation of the same administration, let’s dig into what we learned from the report!

The quantity of debt to be issued

The first half of the QRA came on Monday when we received an update on the amount of debt the Treasury plans to issue for the upcoming quarter.

The Treasury anticipates the following:

For October – December 2024:

- Targeting a Treasury General Account (TGA) drawdown from the current $886 billion to $700 billion.

- During this time, Treasury plans to issue $546 billion in net issuance.

For January – March 2025:

- Targeting a TGA balance of $850 billion, up from the previous quarter that anticipates $700 billion.

- Net borrowing of $823 billion.

The numbers reflect a significant increase in debt issuance planned for the next couple of quarters — an increase of $277 billion. That said, the decrease in the TGA balance explains $150 billion of that marginal requirement.

The composition of debt to be issued

The real juice of the QRA comes from getting a pulse on what the maturity profile of the debt issuance will be (essentially, how much of each maturity will make up the total borrowing amounts).

We can see the composition of debt for the next two quarters below:

A few key insights here:

- Treasury Secretary Janet Yellen has provided guidance that there are no plans for any change in long-duration issuance composition in the coming quarters. Effectively, the dollar amount of issuance for anything longer than one-year of duration is set to remain constant.

- This means if borrowing needs increase, it is up to issuance of less than a year (T-bills) to take up the mantle of issuance.

- Because of the incoming TGA drawdown to $700 billion, then reversal to $850 billion, a substantial increase in bill issuance will be required to fund the Treasury.

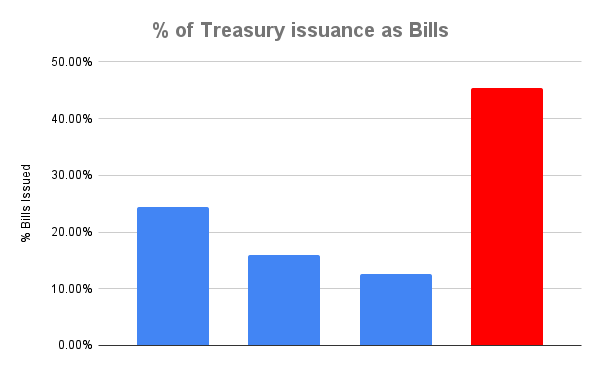

When we look at the proportion of total net issuance in recent quarters that is T-bills, we get the following:

Of note, the Treasury is forecasting an increase of proportion from 13% to 45%. This is notable, as historically the Treasury targets a long-term average of 15% to 20% of total debt being T-bills. Admittedly, this 45% weighting is likely an outlier that will be reversed in Q2 2025 when tax receipts come in and dampen the requirement for bills to take up the issuance mantle.

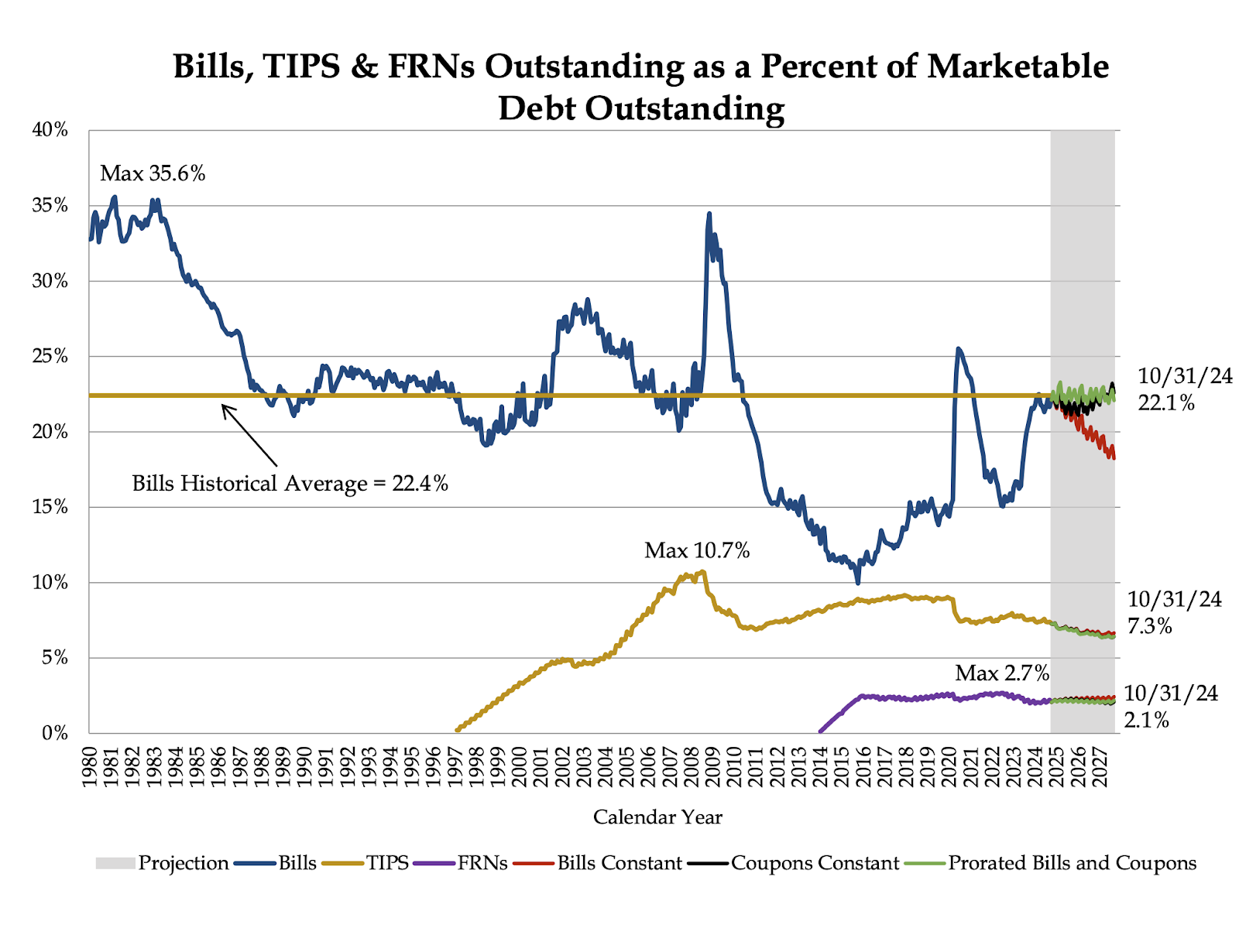

That said, with total Treasury debt outstanding already above the upper limit of their target range at 22%, one must wonder how long this game of avoiding surprising markets with duration can last:

Read the full article here